Published March 29, 2022

Credit unions have grown their mortgage origination operations and market share over the years, to the benefit of their members and organizations. Unfortunately, many credit unions and community banks have not given proper attention to a form of interest rate risk that accompanies this unique area of the business. This article explores the significant financial risk credit unions and community banks accept when issuing an interest rate lock commitment (IRLC) to a member/borrower who has applied for a mortgage, and strategies to mitigate that risk.

As the largest mortgage interest rate risk management (i.e., hedging) advisory and technology provider in the U.S., Optimal Blue, a division of Black Knight, has developed keen insights and understanding of the best practices and strategies of leading mortgage institutions across all business types. This includes many of the largest and oldest credit unions and community banks in the country. Our capital markets team meets with credit unions and community banks located across the U.S. daily, and provides actionable ideas for implementing IRLC risk management strategies.

Rate Sheet Strategy

Many, if not all, credit unions and community banks we encounter employ some sort of rate sheet pricing strategy that considers two key aspects.

First is the competitive landscape, which is typically ascertained by having staff perform a daily surveillance of competing similar institutions – literally by visiting competitor websites and obtaining generic price quotes. More advanced mortgage operations will use a market surveillance tool, such as Optimal Blue’s Competitive Analytics, to view real-time, actual rate/fee offers, thus obtaining a more granular and accurate view of the market competition.

The second aspect is the acceptable revenue per loan required by an institution’s mortgage pricing strategy, inclusive of fee income and anticipated loan sale revenue. The revenue target is typically prescribed by the CFO, treasury department or executive committee. Interest rates are determined by the corresponding price that incorporates a premium, or margin, above the par price from the source. The pricing source for anticipated loan sale revenue is typically the then-current price offered by the government-sponsored enterprise (GSE) – e.g., Fannie Mae or Freddie Mac – to which the institution intends to sell its loans.

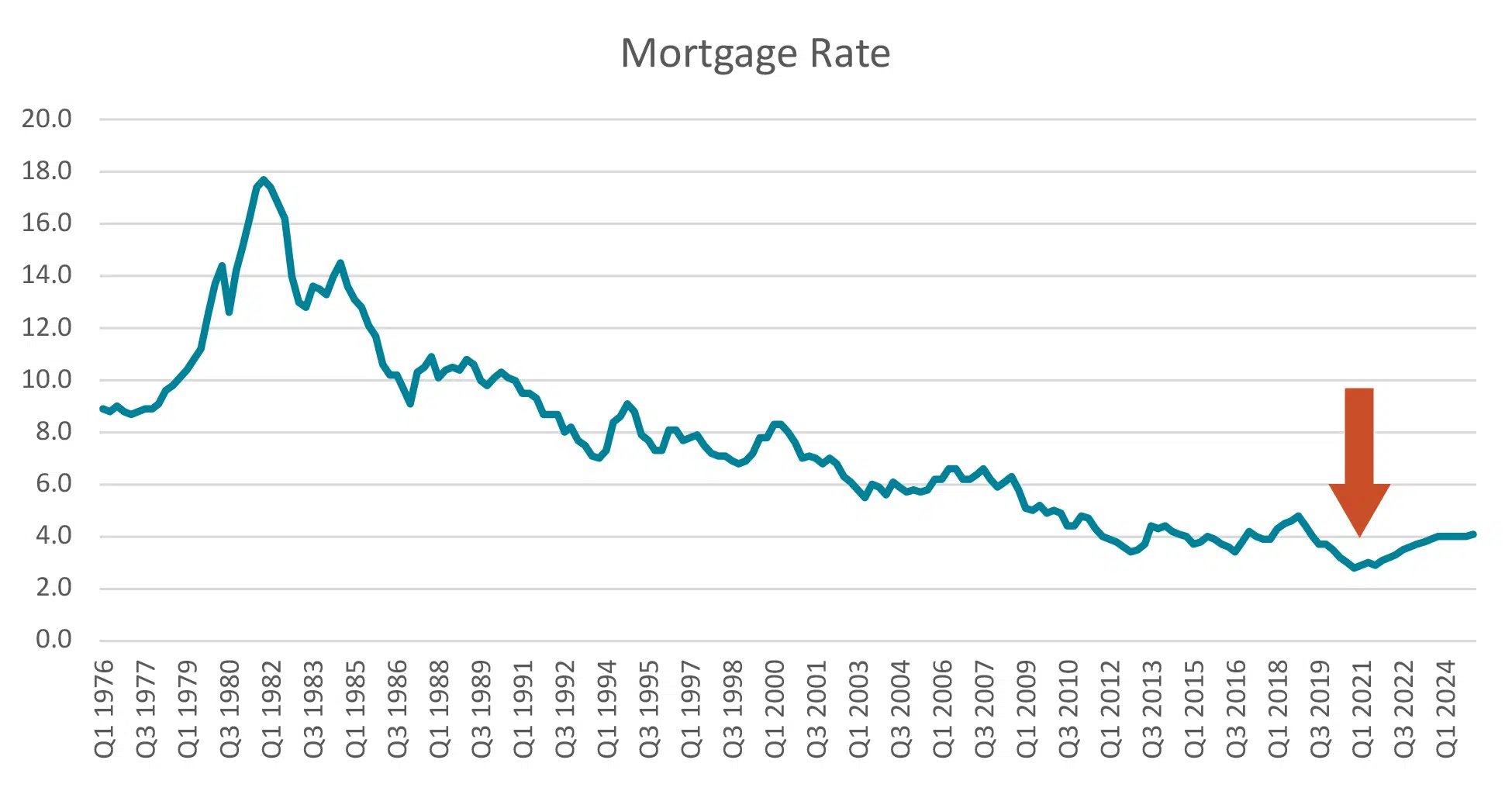

Fixed Rate Mortgage Trend

For much of recent history, mortgage rates have been on a decline, but as of Quarter 1 of 2021, we’ve begun seeing mortgage rates moving counter to that long-term trend. While “floating” a pipeline of IRLCs during periods when mortgage rates are stable or declining can be a relatively benign activity, doing so during periods of rising rates (i.e., deteriorating prices) can have material – even severe – impacts on the financial performance of your mortgage operations and institution at large.

Figure 1

If I Don’t Report on it, it Didn’t Happen

It’s not uncommon for us to encounter institutions with balance sheet capacity that simply ignore IRLC risk altogether. These organizations take closed loans that may have been originally designated for sale to one of the GSEs, and instead hold them in their portfolio. Even though the IRLC may have been issued at an interest rate that would have yielded a price of, say, 101.5, once the loan is closed and ready for sale, the current market is, say, 99.5. No one wants to record a loss on their origination business, so they recategorize the loan as held for portfolio and begin servicing it. The forgone 200-basis-point opportunity cost is not recognized, much to the long-term detriment of the institution.

Some other common strategies employed by credit unions and community banks to mitigate the risk of IRLC pipeline value deterioration include:

- Delay acceptance of IRLC until member/borrower loan file has reached an advanced milestone (e.g., underwriting approval)

- Only then take either a best efforts or mandatory loan-level commitment at the cash window with the required lock period for closing and delivery

| PROS | CONS |

| Reduces the number of days of exposure to market movement risk | Retains some fallout risk Requires additional loan-level lock change management throughout the loan processing, underwriting and closing stages |

| Reduces the likelihood of fallout and the attendant pair-off fees | Less competitive strategy versus institutions that provide the member/borrower the security of an IRLC at time of application (i.e., provides a sub-optimal member experience) |

- Only lock loans with the cash window on a best-efforts basis

- This results in the institution forgoing the available mandatory delivery price premium, as well as additional significant price incentives for lower-balance loans

| PROS | CONS |

| Transfers the market movement risk from the originating institution to the GSE Eliminates the need to closely manage loan pull-through | Best-efforts price drop of ~20–30 basis points (avg. $750 on a $300k loan) Forgo most or all of the low-balance specified pay-ups – another 30–80 basis points Requires additional loan-level lock change management throughout the loan processing, underwriting and closing stages |

| Less competitive strategy versus institutions that deliver mandatory and can therefore price more aggressively |

- Issue an IRLC at member/borrower request as early as time of application and then:

- Process and fund the loan, typically a 45–60 day period, and then take either a best efforts or mandatory loan-level commitment at the cash window with the minimum required lock period for delivery priced at current market – which may be substantially different than market at the time the IRLC was issued to the member/borrower

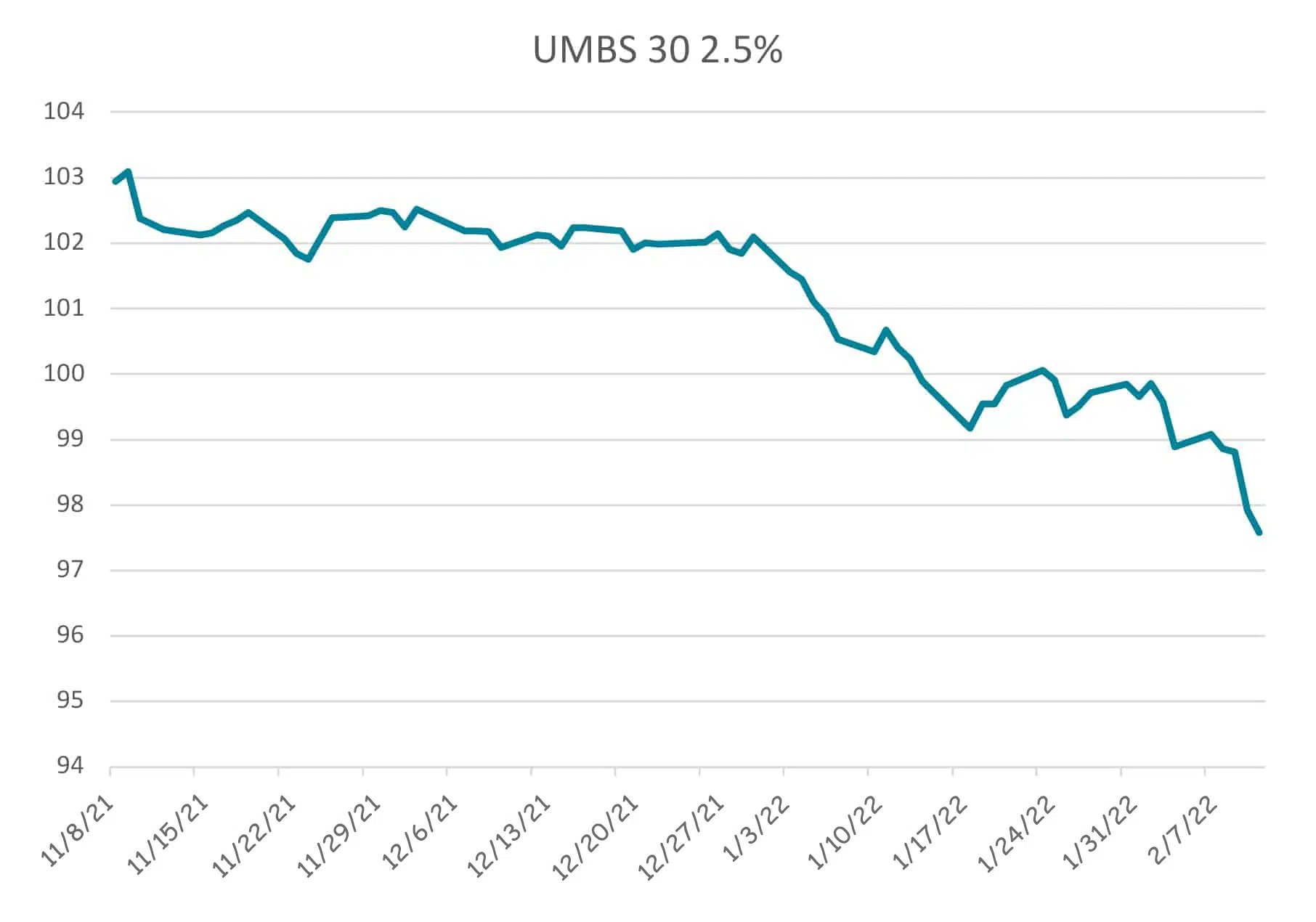

This last scenario is anecdotally the most common. For an example of the ramifications of this exposure strategy, we looked at several aggregate pipeline sizes over a recent 90-day observation period and analyzed the financial impacts to the IRLC-issuing institution.

First, we focused our analysis on the most common mortgage type – 30-year fixed-rate conventional conforming loans. We then chose the most prevalent, or par, coupon during the period, which was the UMBS 30-Year 2.5% during the time of our study.

Figure 2

Exposure Strategy Gone Wrong

As Figure 1 illustrates, we have enjoyed a long-term trend of declining mortgage interest rates (and inversely, the increasing value of the mortgage asset) since 1982, with a few notable bumps along the way. But now that rates are starting to tick up from essentially zero, accompanied by nearly record-low unemployment and rising inflation, it appears that the set-up favors increasing rates – at least in the short and intermediate term. Thus, where an exposure strategy has potentially paid dividends during this period – with the exception of aforementioned bumps – mortgage origination operators face the very real likelihood of sustaining losses on their open IRLC pipelines in the anticipated rising rate environment, as illustrated in Figure 2.

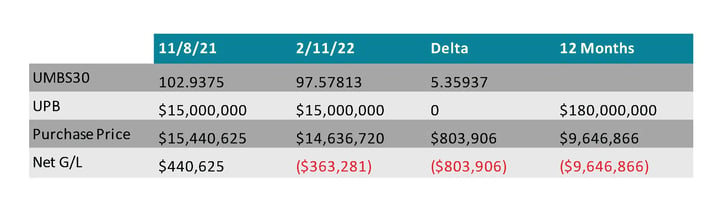

Example

We looked at a base case of a credit union that closed $15 million of mortgages for sale to Fannie Mae, allowing for 66 days to process, fund and deliver the loans. This represents 66 days of market exposure from the day the credit union issued a 60-day IRLC to the member/borrower. For simplicity, we are assuming 100% pull-through in this example.

To be fair, the recent drop in price/rise in rates was a strong one, though hardly unprecedented, and it’s not likely to persist month after month. However, if we assume an approximate 40-basis-point change in price to correlate to a 0.125% change in note rate, we could see an approximate rise of 1.625% in rates from their 2.75% bottom to around 4.375%, an undesirable, but not unthinkable scenario.

Recommendations

With the right IRLC risk management strategy in place, it is possible to both offer your members/borrowers the opportunity to lock in their mortgage rate at the time of application and realize the full, day-one anticipated revenue at the time of loan sale. To accomplish this, credit unions and community banks need to implement a mandatory delivery process that’s accompanied by a risk management (i.e., hedging) program, preferably with both being supported by a single technology platform.

Implementing such a program doesn’t have to be onerous. An experienced hedge advisory service can help guide the process for credit unions and community banks. Here a few of the key considerations.

Understand, Account for and Manage Pull-Through

In many of the credit unions and community banks we visit, there is little, if any, attention paid to measuring pull-through. Fallout (i.e., the inverse of pull-through) is simply considered a cost of doing business, resulting in unnecessarily large pair-off charges and adverse market exposure costs, as in our example above. However, with the proper historical analysis using data from the loan origination system (LOS), a pull-through model can be built to provide a highly correlated indication of current and future pipeline pull-through performance.

Manage Agency Commitments Holistically

When managing IRLC risk using forward commitments, we do not manage them at the loan level. Rather, we use larger “bulk” commitments calibrated to the anticipated pull-through pipeline volume, since multiple loans may be delivered into a single commitment; Fannie Mae refers to this as commingling – there is a significant reduction in time spent managing individual lock commitments.

Automate, Automate, Automate!

Having the right technology in place to efficiently manage the IRLC pipeline is critical to fully realizing its revenue potential, while also reducing the staff time required to manage it. It is common to see personnel in the mortgage department working with the individual rate locks in the LOS, and then someone in the treasury department responsible for managing those same locks as commitments with Fannie Mae/Freddie Mac in their respective systems. Layer on the numerous spreadsheets developed to keep track of and report on all of this activity – and you begin to see how this lack of automation leads to inefficiencies and a higher risk of error. Implementing a true hedge technology platform helps lenders gain the advantages of integrations with the LOS and the GSEs, while also providing a single source for managing the IRLC pipeline activity and producing needed reports.

Result

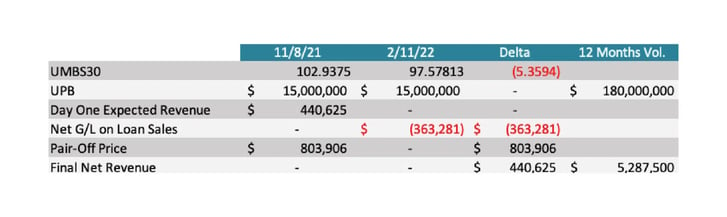

So, let’s examine our base case example of a $15 million pipeline intended for sale to Fannie Mae. We’ll keep the pull-through at 100% for illustrative purposes. But this time, we will employ a hedge strategy using Fannie Mae forward commitments.

The scenario remains the same for the loan sale values, but because we created a hedge position on Nov. 8 using Fannie Mae bulk forward commitments, we were then able to close out that short position on Feb. 11 at the Nov. 8 price. Thus, the original day-one economics are realized – bringing in $440,625 of net revenue from the loan sales. Note that in this simplified example, we have not considered certain fees and revenue, including any potential cash-back pair-off fees and low loan balance pay ups. While not immaterial, these fees and revenue opportunities do not change the conclusion that the economics of managing the institution’s IRLC price risk exposure are hugely positive.

Conclusion

These practices reflect what we have observed over the course of hundreds of meetings with credit unions and community banks across the country – all of different sizes and with widely varying mortgage production volumes. To be sure, many credit unions and community banks do employ a risk management strategy to protect their day-one rate sheet price from the volatility of the secondary mortgage market. The best institutions have invested in the technology and knowledge to automate and standardize processes, to yield not only the optimal financial results, but to produce a better member experience or customer journey for the long haul.