23 April, 2020

Published April 23, 2020

During these unprecedented times, we are all trying to stay safe and healthy. Among other measures, this means a lot of social distancing and time spent in your current place of residence. The purchase market is slowing as both supply and demand are likely depressed by a combination of preventative health measures and economic uncertainty. Those who are concerned about the virus are unlikely to open their home up to open houses or other traffic associated with selling their home, and likewise, are unlikely to expose themselves by shopping for a new home.

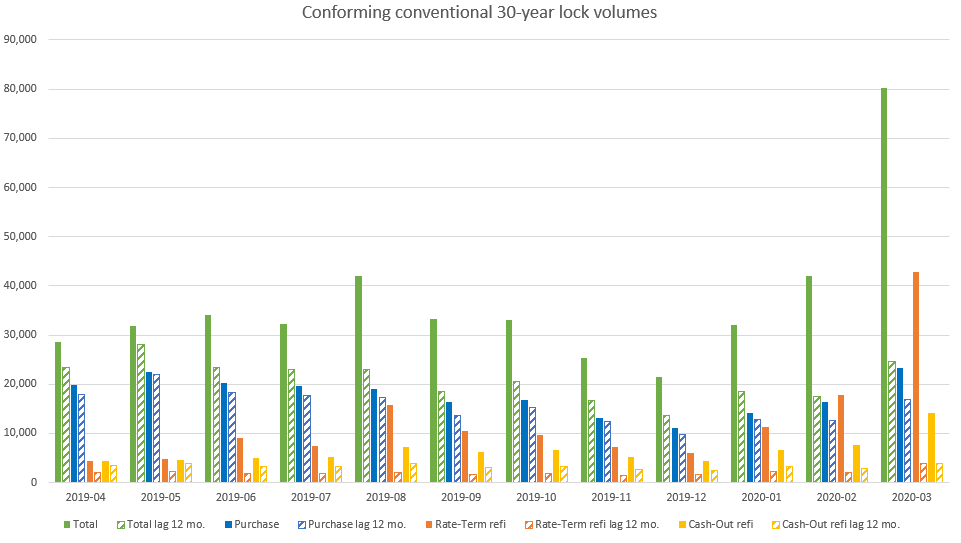

That is not to say that there isn’t any volume. On the contrary, there is extraordinary amount of lock volume. Purchase numbers are up some relative to last year, but both rate-term refinance and cash-out refinances have seen their volume explode recently. However, this booming volume, caused partially by low rates, and partially by economic uncertainty, must be viewed through a more holistic lens because it is likely that a smaller percentage of loans than “normal” will make it from locked to funded.

How is the pipeline impacted by laid-off or furloughed borrowers and to what extent is that likely to impact pull-through? We are seeing a record number of locks, but will that necessarily translate into a record number of loans? There are some administrative hurdles to overcome in order for the lock to become a loan:

| Appraisal, this requirement has been eased somewhat by the new Fannie Mae/Freddie Mac guidelines on accepting external only or desktop appraisals for most mortgages. | |

| The second requirement is only allowing verbal confirmation of employment to close the loan. With business not quite operating as usual, this is a helpful measure, but it can lead to decreased pull-through if large numbers of borrowers are laid-off. | |

| Finally, many purchase agreements are made contingent on the sale of another property – usually the buyer’s current home. As some start having trouble selling their homes, that tends to ripple through the local markets. If originations are geographically clustered or this ends up as a nationwide phenomenon, pull-through rates could again be impacted. |

There is also a potential issue where loans are likely to be subject to repurchase, even if originated by FNMA/FHLMC guidelines, if they go into forbearance within 15 days of being sold. This represents a significant cost to the lender first in repurchasing the loan, then servicing and making the necessary advances on the loan during the forbearance period. Additionally, Fannie Mae is now forecasting purchase numbers to decline by 14.7% in 2020 due to the pandemic and lingering impacts. This is unsurprising but may cause significant headwinds for originators during the prime “home-buying season.”

As you can see, lock volumes are substantially above where they were last year. Even if pull-through falls off a bit, these are still extremely strong volume numbers. When planning goals and budgets, it would be unwise to continue to rely on incredible volumes, as the economic pressures of the pandemic take their toll on households and many of the existing mortgages will already have extremely low interest rates. While the volume is still strong for now, there is always the threat that these headwinds could prevail and set the housing market on a vicious cycle where more borrowers struggle to get employment verification, make payments, and sell their homes. The harder it starts to become for others to do those same tasks, potentially leads to another housing bust. These factors and many others in the global economy indicate that there may also be a volume correction in the other direction leading, to some lean quarters in the near-term. There are also some long-term concerns about volume to be aware of – the first is that there may just be burnout as so many in the economy have already or are currently refinancing. There is another lingering long-term question floating around regarding those borrowers who are taking the forbearance option. While borrowers are not being reported as delinquent during the forbearance period, it still poses some problems for refinancing and potential eligibility. The outlook for mortgage originations will begin to emerge as the FHFA and the GSEs provide clarity around these topics in the coming weeks and months.

BACK