03 December, 2019

When an interest rate on a mortgage is locked with the borrower, the loan origination process is far from complete or pre-determined. Circumstances may arise that jeopardize the likelihood that the loan will close. The underwriter could find the borrower to be unqualified, a home sale may fall through, rates may change, or the borrower could find a better deal elsewhere. These possibilities are important to consider when originating and/or hedging a loan, as they all contribute to what is known as lock “pull-through,” which is often quoted as the percent of locked loans that eventually close. Conversely, “fallout” is the percentage of locked loans that do not close. These percentages are determined somewhat by chance, so predicting them can be tricky. The chance of predicting poorly poses a risk to the originator if committing via mandatory, and potentially the investor if selling loans via best efforts. In the latter scenario, the pull-through risk is assumed by the investor. Further, the costs in terms of staff time to lock, underwrite, and advance the lock through the loan process is wasted if the lock does not pull-through.

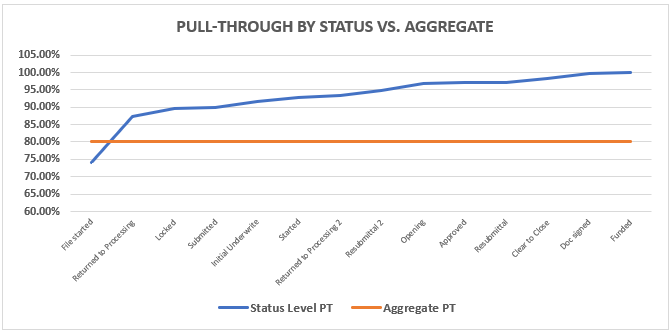

The most crucial adjustment in any hedge position is the adjustment for pull-through. This key variable is paramount to ensuring a hedge that isn’t unnecessarily incurring hedge cost on loans that won’t fund. The simplest way to analyze pull-through is an aggregate, entire pipeline analysis. Meaning, funded loans divided by total locked loans equates to the pull-through percent. This base measurement of pull-through is useful for informational purposes but analyzing available data in a more granular way will allow for more precise pull-through assumptions. One of the most common and reliable loan attributes used to determine probability of a loan closing is current loan status. Loans are more likely to pull-through as they move from status to status through the origination process. One even more detailed component of status level pull-through is the operational time it takes for loans to fund or cancel. An analysis incorporating this aspect of the life cycle of the loan will highlight the impacts of leaving cancelled loans in the pipeline longer or waiting to clear out “dead wood” until month-end. Each meaningful level of granularity allows for further refinement in the total pull-through metric that is used in the shock position and further increases the shocks’ accuracy. It’s important to note that any pull-through analysis relies heavily on historical data (6 months to a year’s worth, at least), which can be used to help predict future pull-through performance.

Simply put, hedging loans that will cancel, or “over-hedging,” is a losing game. In fact, you’ll end up eating a lot of excess hedge costs, such as dealer spreads, even if the market doesn’t move at all. Now include market risk on your over/under-hedged amount and you could be sitting on some very unsavory numbers. For example, if you are over-hedged as prices are increasing, you’ll face large, negative market movements on the coverage you had open, and no loan gains to back that up. The same can happen in the inverse of being under-hedged in a sell-off, you will have loan losses that won’t have matching coverage gains. These implications, only expounded by the size of the market move and the degree to which your pull-through assumptions are wrong, highlight that maintaining an accurate pull-through model is critical. Monthly auditing of your model will allow for minute adjustments based on market conditions, pipeline mix, and any operational changes that may have affected pull-through performance.

The example above displays how pull-though varies as a lock moves through the loan life cycle. It is plainly visible that an aggregate analysis or constant pull-through assumption (typically at 80%) does not capture the intricacies of the system very well and therefore, a relatively sophisticated pull-through analysis increases accuracy, and should improve hedge performance, assuming that the percent of the pipeline in each status is not constant. Depending on your business model, investing in a sophisticated hedging partner can make a real impact on the bottom line.

BACK